Maitri — fixing the unspoken bottleneck in Indian agriculture.

A $9.1B machinery market. 70% of farmers cut out of it. A second Masters' Union Startup Weekend pitch in 2023 — this time, the problem wasn't taboo, it was just invisible. Small and marginal farmers own 85% of India's farmland and have almost no access to agricultural mechanisation. Maitri is the rental layer that fixes it.

The numbers tell a story India doesn't talk about.

The machine at the center of the problem. 70% of India's small and marginal farmers own no tractor. During peak sowing windows, 50% of them cannot get machinery on time.

70% of India's farmers are classified as small and marginal. Between them, they own about 85% of the country's farmland. And almost none of them — about 10% — own a tractor. When their crop window arrives and they need machinery to plough, sow, or harvest, they either pay through the nose for ad-hoc rental or wait, lose yield, and absorb the cost in their margins.

The headline statistic from the original problem statement: during sowing windows — when machinery demand peaks — about 50% of small and marginal farmers don't get quality service on time. That's a structural productivity loss baked into the entire agricultural economy.

Why this is invisible

Unlike urban consumer problems, this one doesn't show up on Twitter. The farmers most affected are least likely to be talking about the problem in venues that fundraisers read. The machinery rental market has no major players. The space is open precisely because the people in pain don't have the megaphone.

$9.1B and growing — with no consolidated rental layer.

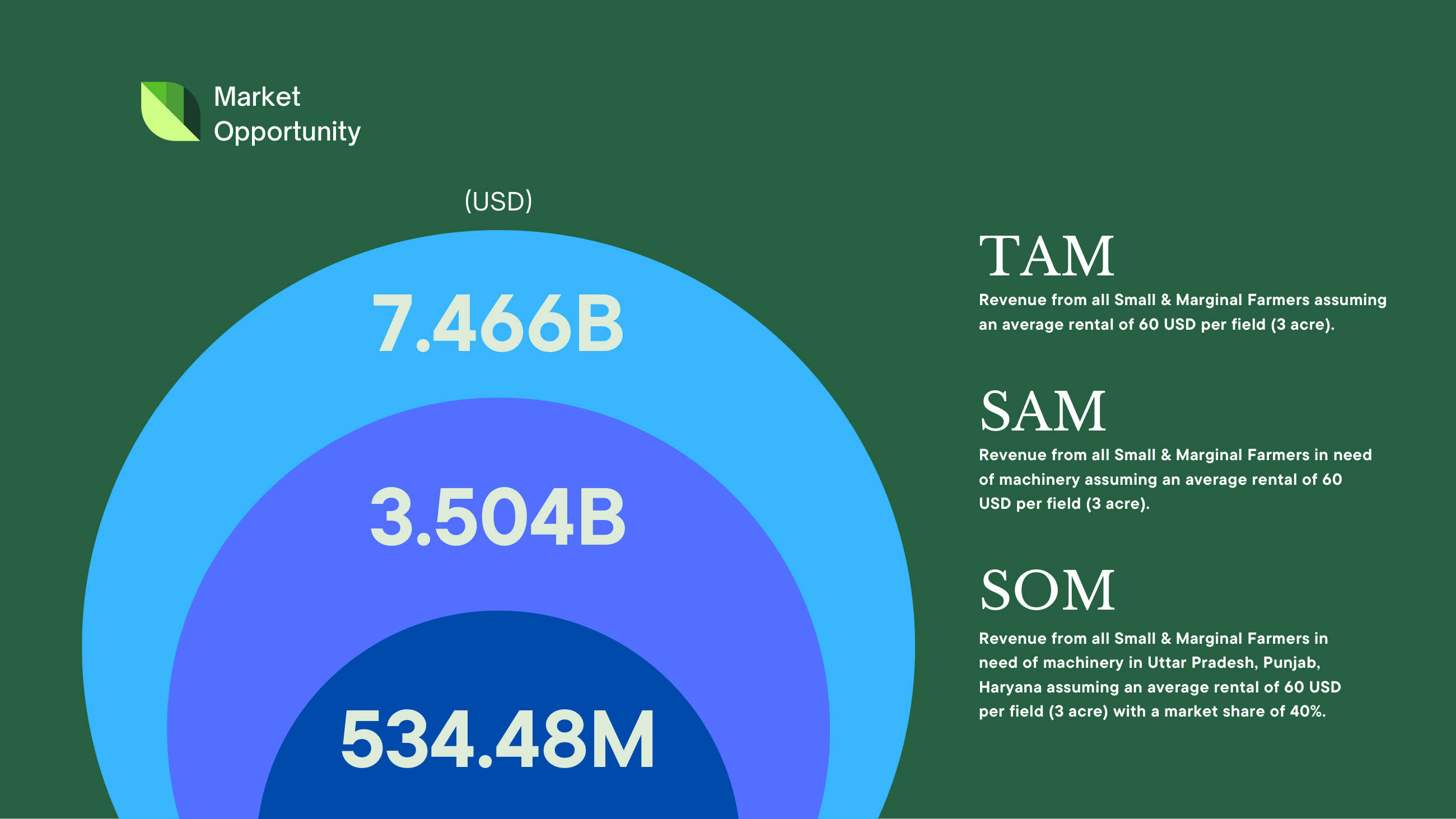

TAM of $7.466B (all small and marginal farmers at $60/field rental), SAM of $3.504B (those actively needing machinery), SOM of $534M targeting UP, Punjab, and Haryana at 40% share over 3 years.

The Indian agricultural machinery market is roughly $9.1B. The rental sub-market — the part Maitri targets — is the under-served slice. The TAM/SAM/SOM analysis worked out as follows:

- TAM — $7.466B. Revenue from all small and marginal farmers assuming average rental of $60 per 3-acre field.

- SAM — $3.504B. Revenue from all small and marginal farmers in need of machinery at the same average price point.

- SOM — $534.48M. Revenue from small and marginal farmers needing machinery across Uttar Pradesh, Punjab, and Haryana, assuming 40% market share — the realistic first 3-year target.

Why these three states

Punjab, Haryana, and Western UP are the agricultural belts where mechanisation demand is highest, plot sizes are workable, and policy infrastructure is most supportive. Concentrating SOM here gives Maitri a realistic foothold before national expansion.

Three layers that turn rental into a real service.

Maitri is a one-stop solution for renting farming equipment on time, in an efficient and optimal manner. Three layers:

1 — Renting agricultural machinery

Equipment delivered on demand. End-to-end service including the operating staff and the logistics to move the machine to and from the field. Tractors, harvesters, tillers — the essentials.

2 — Tele-support

A regional-language support line. Weather alerts, government scheme information, and a direct line to a Maitri representative. The phone is the most accessible interface in rural India — Maitri leans into it instead of trying to force adoption of an app.

3 — Data-driven optimisation

This is the moat. Maitri runs algorithms on demand patterns, cluster geography, and seasonal cycles to figure out where and when machinery should be pre-staged at central hubs. The farmer doesn't wait three days for a tractor to arrive from 200km away — the tractor is already in their cluster, waiting.

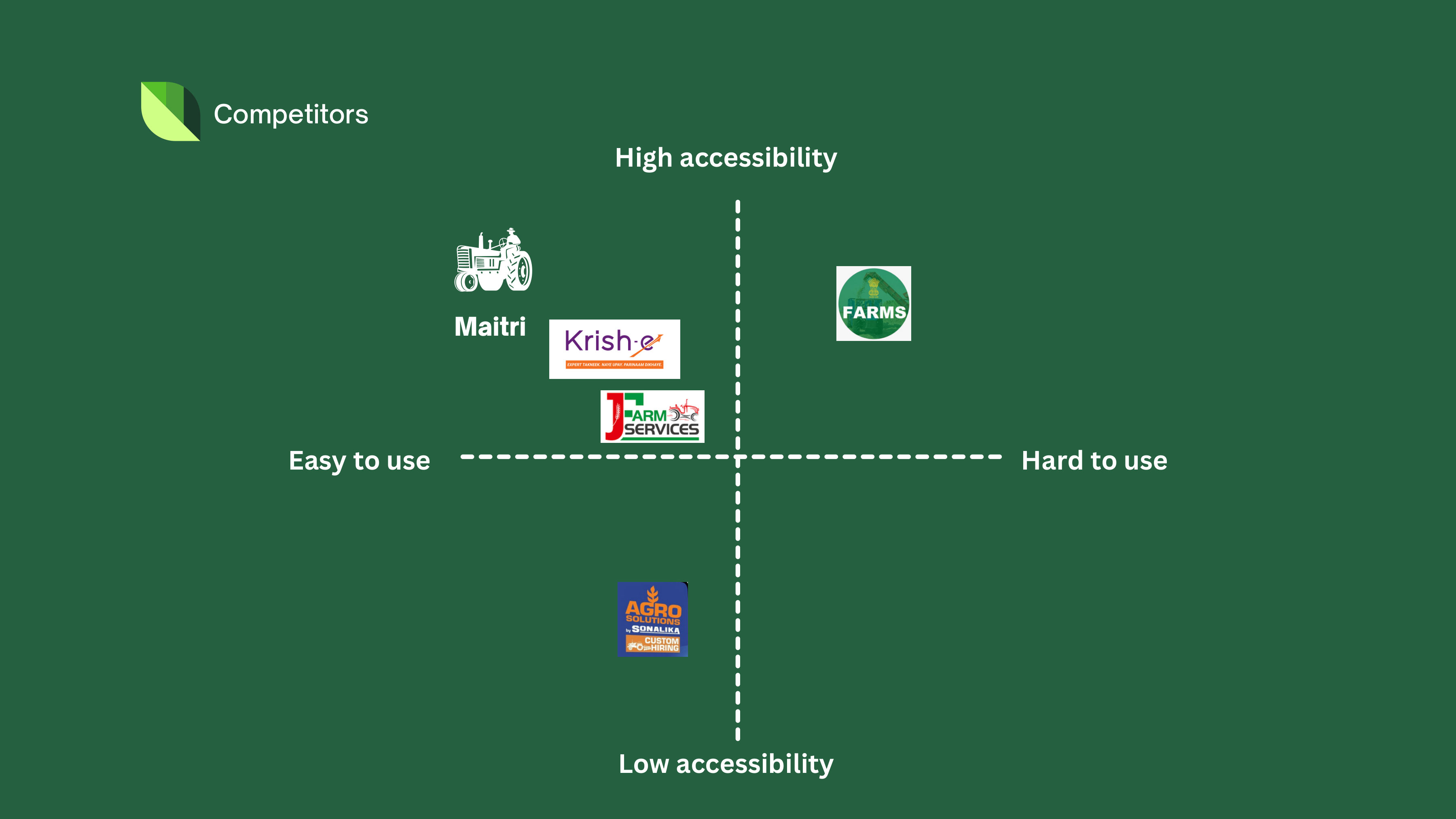

High-accessibility, easy-to-use. The empty quadrant.

The competitive landscape on two axes: accessibility and usability. Maitri is the only player targeting the top-left quadrant — high accessibility, easy to use. Every existing option fails on at least one axis for the small farmer.

The 2x2 map plotted existing players on two axes: accessibility (how easy it is for a farmer to actually access the service) and usability (how straightforward the rental experience is). The high-accessibility, easy-to-use quadrant — the one a small farmer in rural Punjab could actually use — was empty.

Existing competitors clustered into:

- Government schemes — high accessibility in theory, but operationally complex and unreliable in delivery.

- Local entrepreneur-owned tractors — easy to use if you know the person, low accessibility if you don't, opaque pricing.

- National machinery rental startups — easy to use, but app-first models and urban-centric service maps make them inaccessible to most target farmers.

Maitri's differentiator was deliberately structural — phone-first interface, hub-and-spoke pre-staging, regional-language support — not feature gimmicks.

Test small. Optimise. Then scale on data.

Year 1 — Haryana

Start with one state. Stage equipment at 2–3 cluster hubs. Acquire customers through farmer surveys and a hotline number (no app). Measure: utilisation rate per machine, average wait time from booking to delivery, NPS via call-back surveys.

Years 2–3 — Punjab and Western UP

Expand to adjacent agricultural belts. Apply the data from Haryana to optimise hub placement before launch — Maitri should know where the tractors need to be by the time it arrives in a new region.

The differentiators we'd lead with

- Guaranteed service and on-time delivery. The single most important promise. Reliability is the product.

- Customer-friendly model. Phone-first, no app required, regional language support.

- Affordable pricing. Below local entrepreneur rental rates, with transparent fees.

- Data-driven supply chain. Invisible to the farmer; critical to the unit economics.

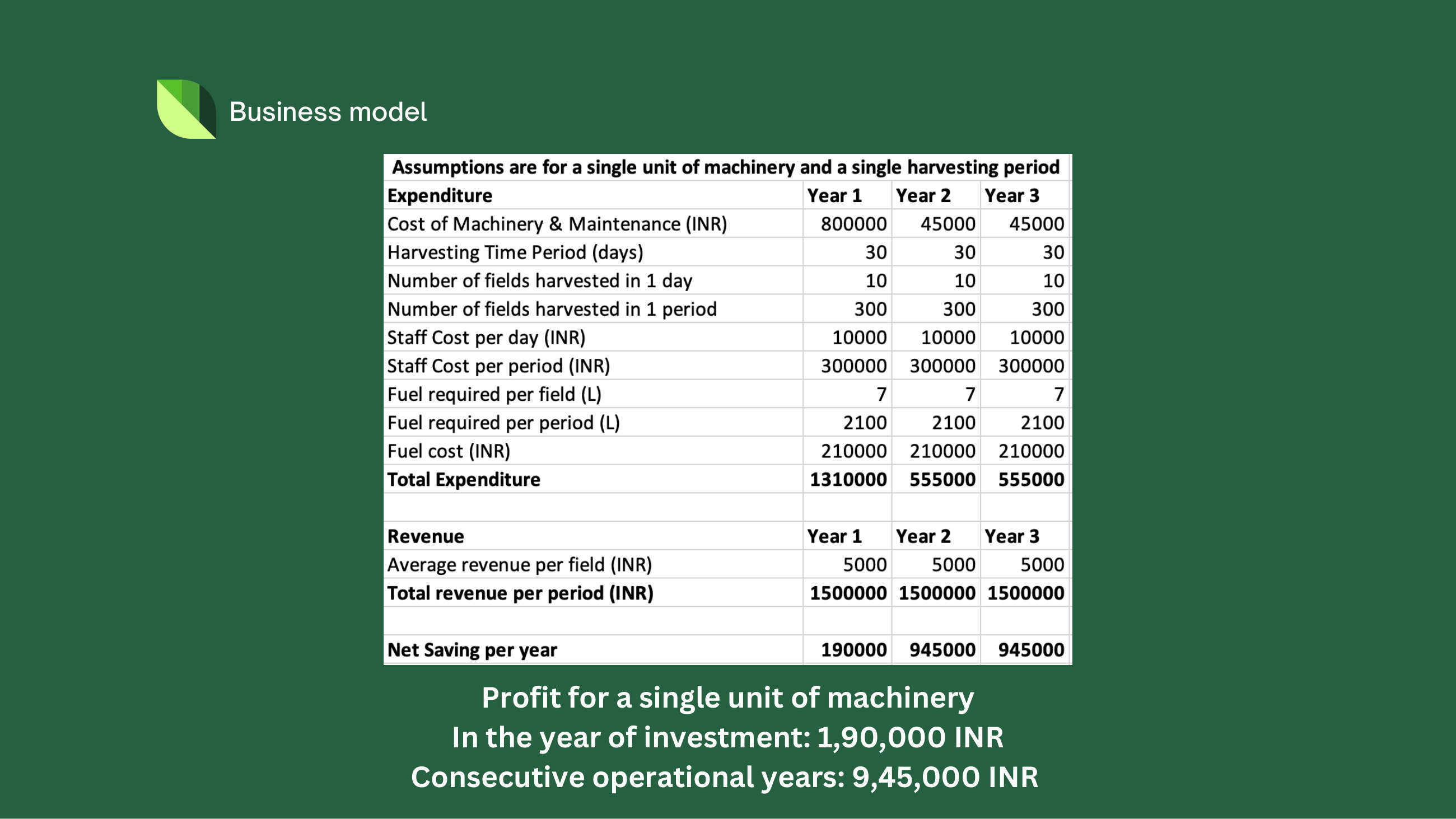

The math that makes this work.

Per-machine unit economics across three years. Year 1 absorbs the ₹8L acquisition cost; Years 2 and 3 run at ₹9.45L net profit each — this J-curve shape is the core investor story.

The revenue model is service-based. Each machine type has its own rental price; each is rented some number of times per season. Total rental = (rate per type × times rented) summed across machine types per hub.

Per-unit profitability

- Year of investment: ~₹1,90,000 profit per machine unit (after acquisition cost amortised against utilisation).

- Consecutive operational years: ~₹9,45,000 profit per machine unit (acquisition cost fully absorbed; pure operational profit).

The headline insight from this math: Maitri's per-unit economics are dramatically better in years 2+ than year 1. Which means the business is most fragile when capital is freshest and gets sturdier as utilisation compounds. Investors care about that shape.

What I learned, putting this on a slide.

Three lessons that have outlasted the deck:

- The biggest markets are often the quietest ones. Agricultural mechanisation rental is a $7B+ space with no major players because the customers don't tweet. The absence of buzz isn't the absence of demand.

- Phone-first is a feature, not a step backward. Building this as a phone-and-SMS product instead of an app-first product would have been culturally suspect at a startup weekend. It's also the only way to actually reach the customer.

- The moat is operational, not technical. The data-driven hub optimisation is a technical advantage. The trust earned by delivering tractors on time, every time, is the actual moat. The technology serves the trust.

Maitri stayed a pitch deck. The thinking — that the cleanest 0→1 opportunities are often hiding in markets where the customer can't be your beta tester on Twitter — has shown up in every fundraising conversation I've had since.